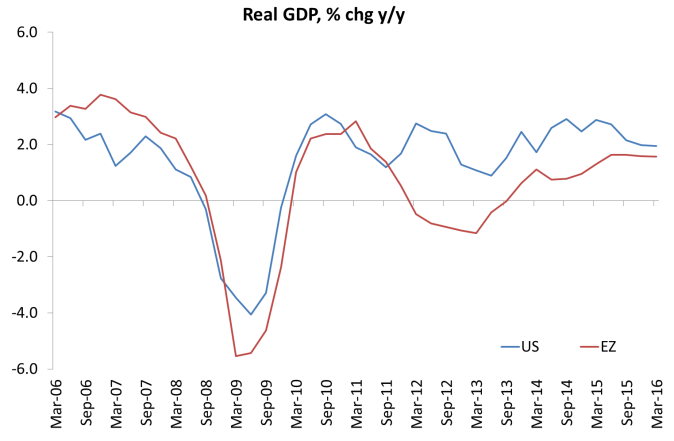

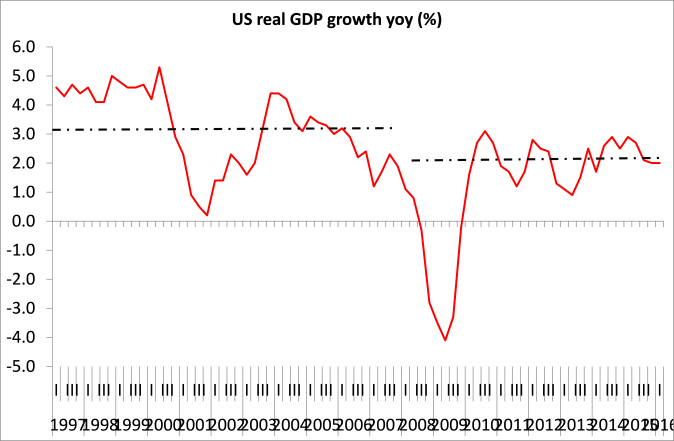

Anyway you look at it, the US economy is slowing down. Indeed, real GDP growth in the US based on the last quarter (Q 2106) has slowed to 1.9% year over year, not much above the rate of growth in the Eurozone. The decline in growth is the product of a decline in investment. The investment drag is clear with GFCF in the Eurozone outpacing its US equivalent for the last two quarters.

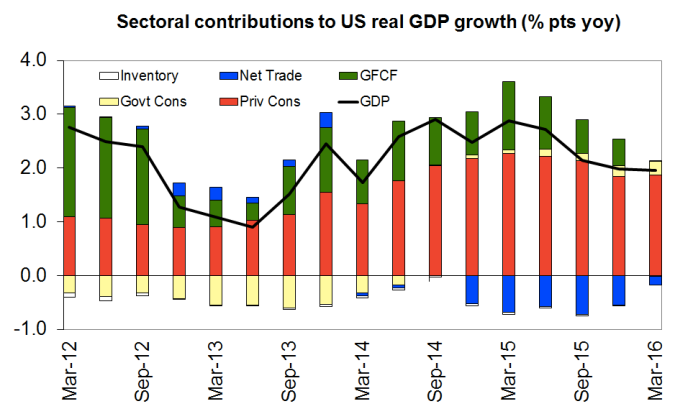

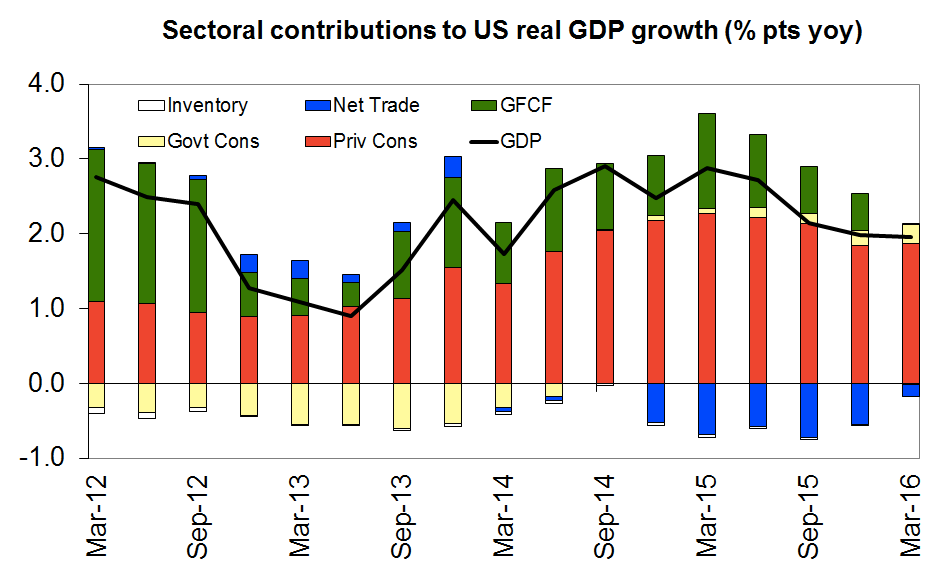

Total investment in the US is now making no contribution at all to the expansion of the economy. See how the green part of the bars below has disappeared.

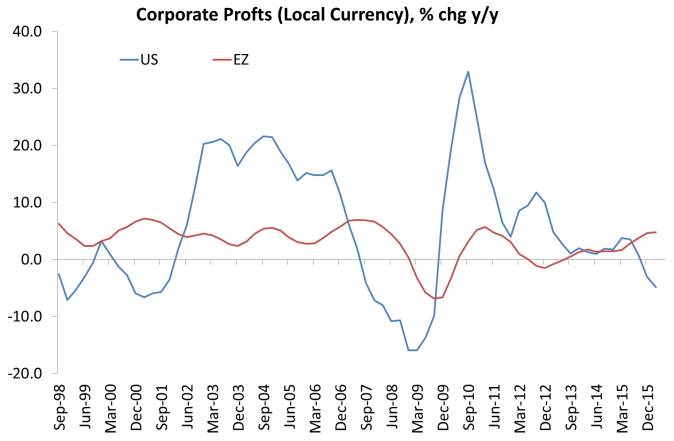

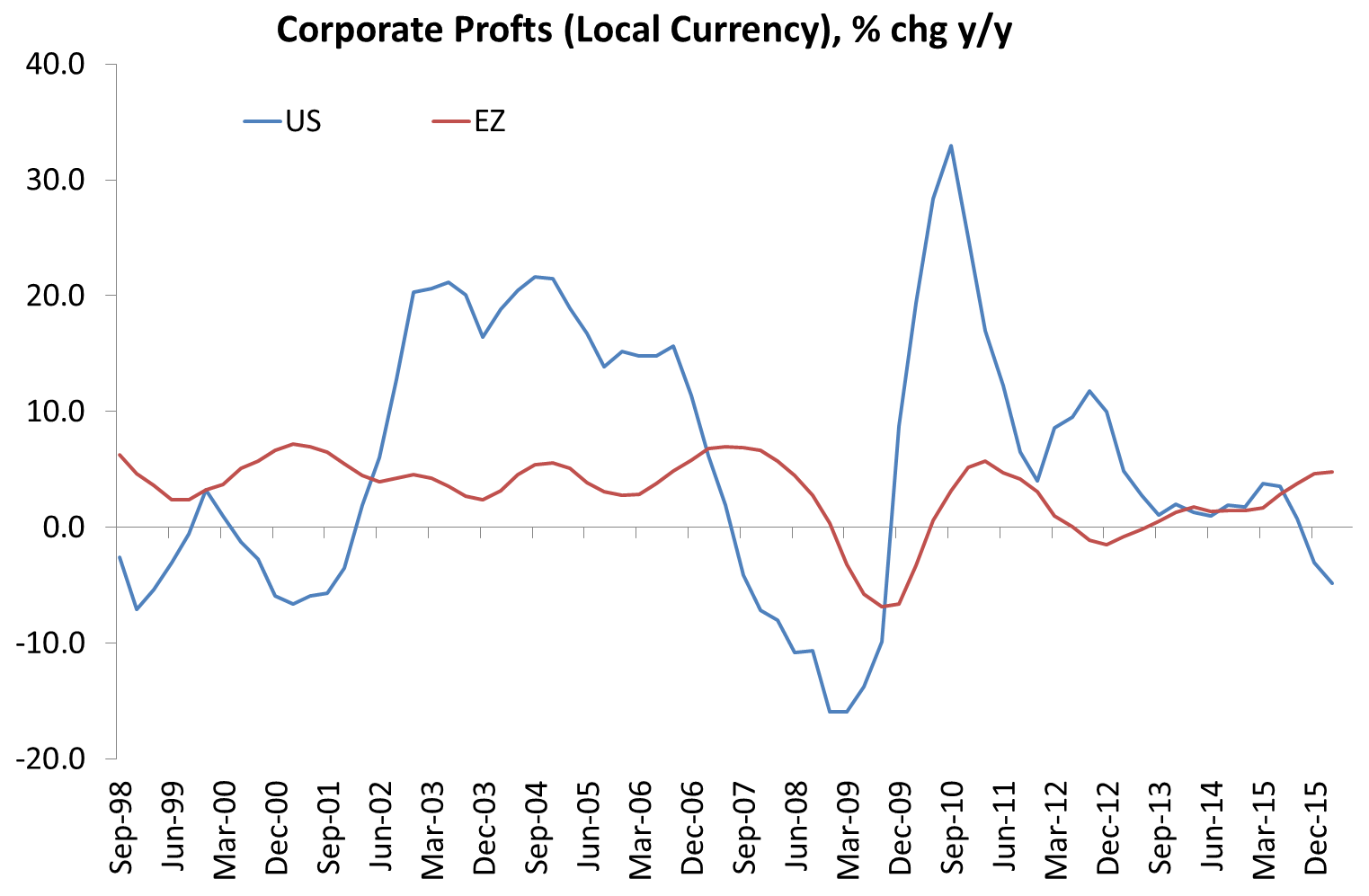

As I have shown before, this weak investment mirrors the deterioration in corporate profitability, which is now falling in the US.

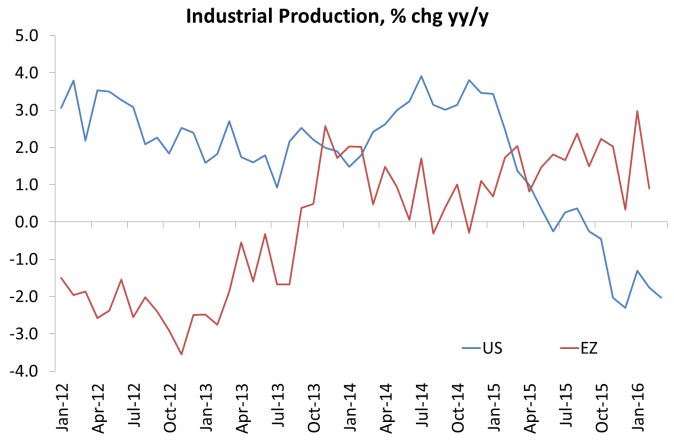

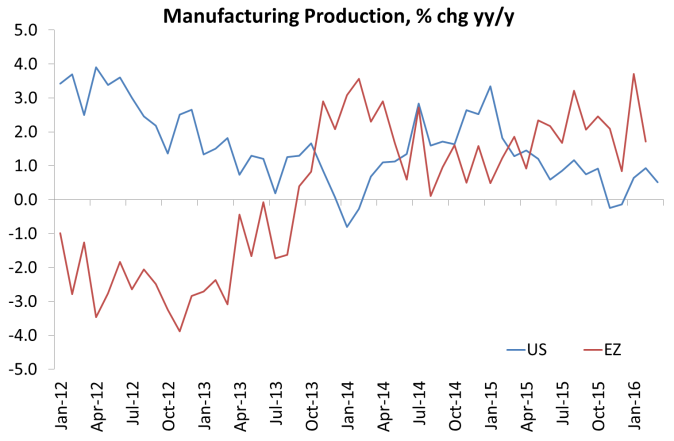

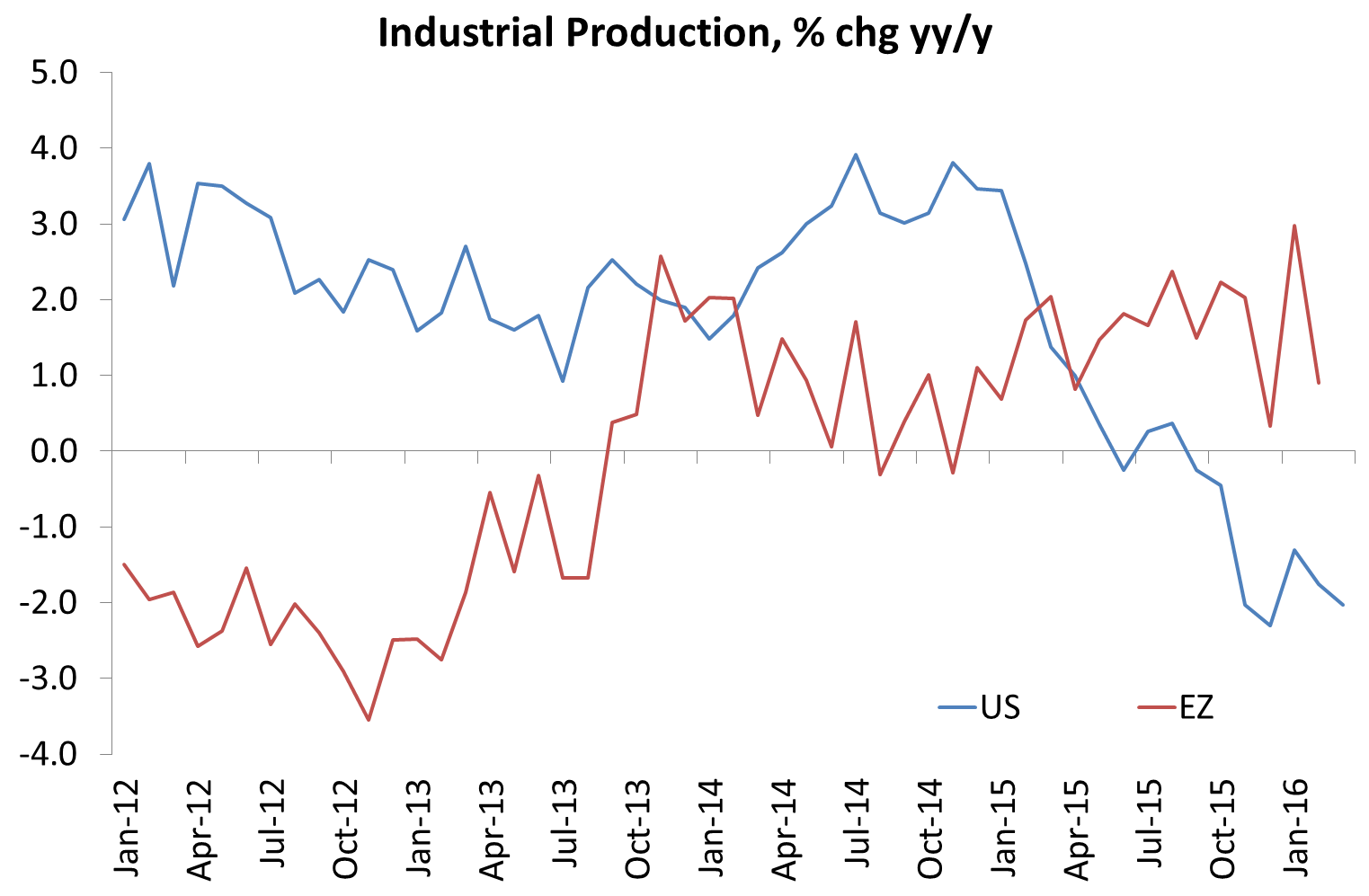

The productive sector of the US economy has particularly weakened and is now heavily contracting – in contrast to weak but steady growth in the Eurozone.

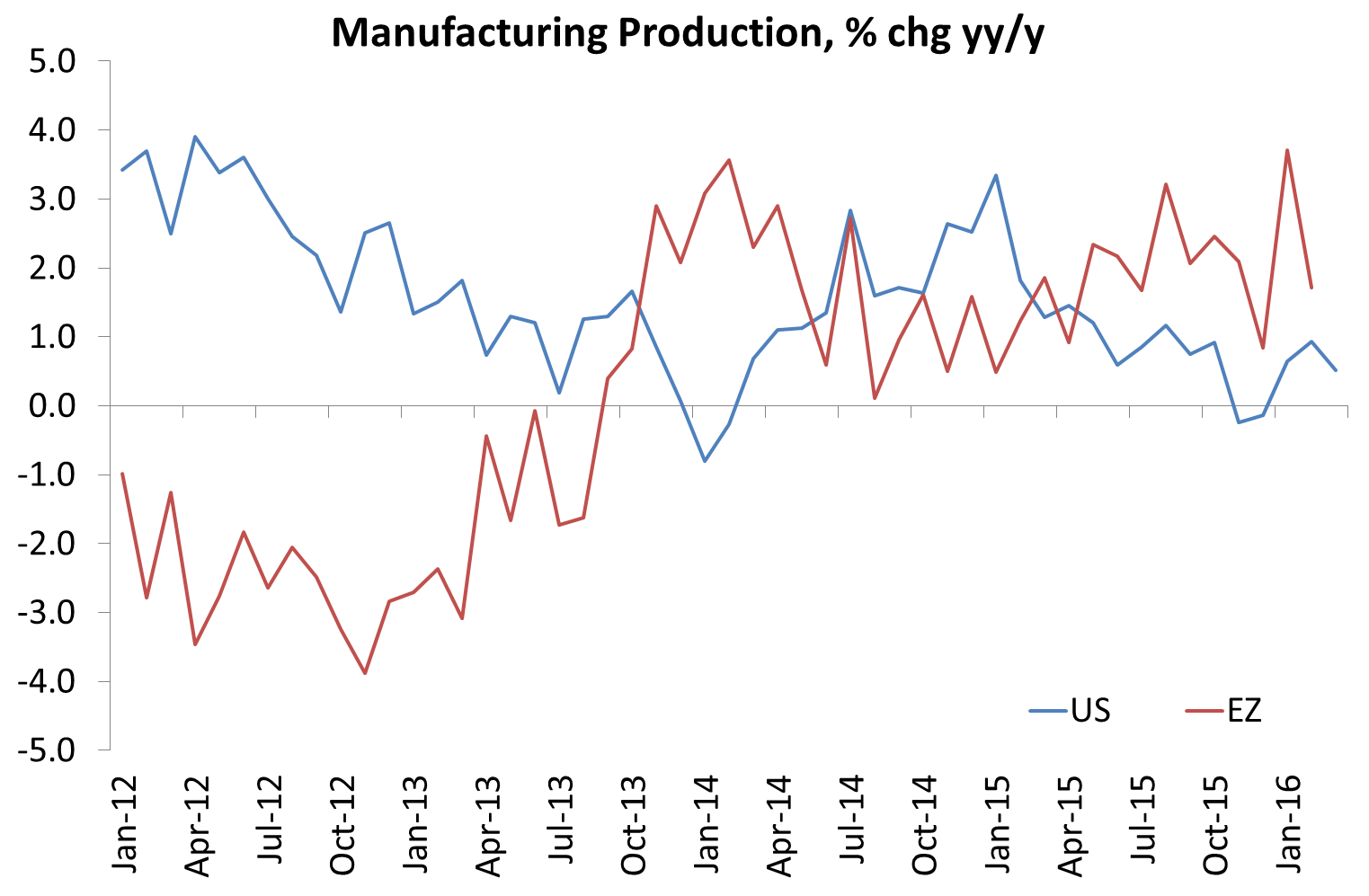

Most commentators argue that this is due to temporary hit to the energy sector following the collapse in oil prices. But even if you exclude energy production, US manufacturing output is crawling along.

Alongside slowing real output, inflation in prices of goods and services has disappeared in both the US and the Eurozone. Deflation is still close – another indicator of the long depression in the major economies.

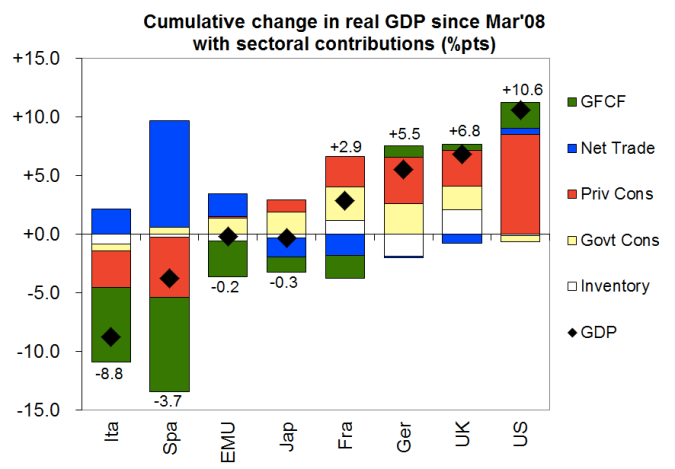

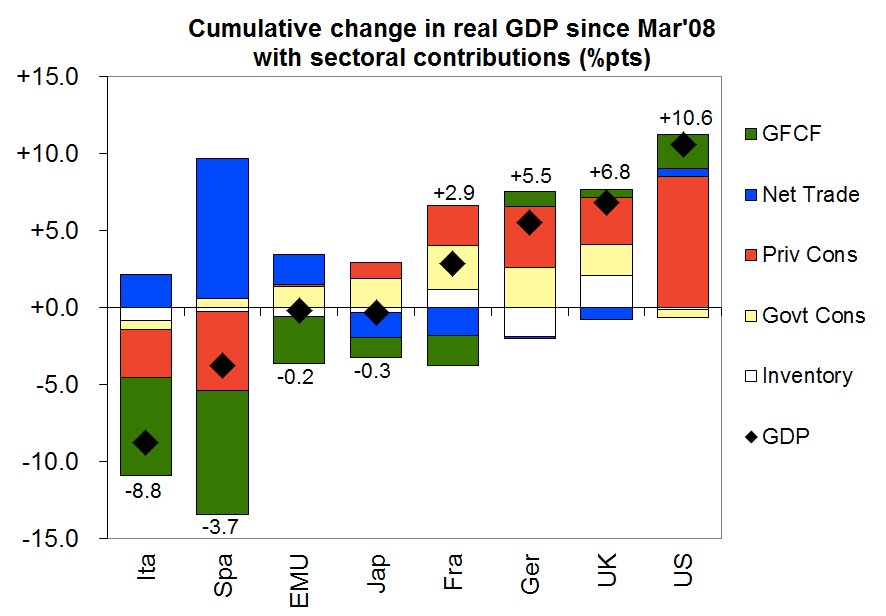

But here is the real irony that should confound the Keynesians who reckon that the cause of the depression is the failure of governments raise spending to compensate for ‘weak demand’. Since 2008, the US economy has grown faster than the Eurozone. And yet in the US government spending has made a negative contribution to that growth while, despite all the talk of German-imposed austerity, government consumption has provided a net boost to real GDP in most European countries since the crisis broke. In other words, there has been more ‘austerity’ in the US than in Europe and yet the US economy has recovered better from the Great Recession!

The graph below shows that since 2008, the US economy has grown 10.8% but government spending (yellow bar) has shrunk, while the German economy has risen only 5.5% with government spending contributing over 2% pts of that. Even ‘austerity’ UK has seen more government spending in its recovery.

Nevertheless, the Keynesians continue to claim that this low growth world is due to the lack of fiscal and monetary injections into the economy andhas nothing to do with the underlying problems of the capitalist economy: low profitability, high debt and weak investment and poor productivity growth. Only this week, Martin Wolf told us, yet again, that weak growth in the Eurozone is due to the failure of Germans to spend or invest rather than save. Germany needs to absorb its ‘excess savings’ by spending to get Europe and the world going.

This is nonsense. As I explained in some detail in a previous post, there is not a global savings glut that needs to be absorbed. And German corporate savings as a share of GDP are not particularly high compared to other countries. The issue is low investment, yes. But why? Wolf seems to think it is due to ignorant, rigid attitudes in Germany and elsewhere. But the objective reason is low profitability from future investments and existing relatively high corporate debt. Another way of looking at this is to say that it is a ‘supply-side’ problem, not one of the lack of demand.

An argument in these terms has broken out between the Keynesians and the neo-classical wing of mainstream economics. A new paper by some top Keynesian economists, couched in extremely obtuse mathematical models, seeks to show that the current weak US economy is due to the inability of central banks to get interest rates low enough to stimulate investment. The US economy is ‘zero-bound’ and so we have ‘secular stagnation’. This is the Summers-Krugman explanation of this long depression.

In response, neoclassical economist John Cochrane has shown that these assumptions are just unrealistic. “I read this paper as a brilliant negative result. It shows just how extreme the implicit assumptions are behind the policy blather. It shows just how empty the idea is, that our policy-makers understand any of this stuff at a scientific, empirically-tested level, and should take strong actions to offset the supposed problems these buzzwords allude to”. Cochrane’s alternative view is simple, he says. Interest rates are low because inflation is near zero. Growth is low because productivity growth is low. Productivity growth is low because investment growth is low so the productive potential of the US economy has fallen back. This is much closer to the Robert J Gordon explanation of the depression.

The policy conclusion of the Keynesian position is to pump yet more money into the banks and the economy (helicopter money next) and for governments to launch spending programmes. The neoclassical supply-side policy position is to make companies more efficient by cutting wages and employment and reduce the ‘regulation’ of the capitalist companies to allow the ‘market’ to work; while cut government spending to reduce the level of debt.

Neither option has worked or will work.

Total investment in the US is now making no contribution at all to the expansion of the economy. See how the green part of the bars below has disappeared.

As I have shown before, this weak investment mirrors the deterioration in corporate profitability, which is now falling in the US.

The productive sector of the US economy has particularly weakened and is now heavily contracting – in contrast to weak but steady growth in the Eurozone.

Most commentators argue that this is due to temporary hit to the energy sector following the collapse in oil prices. But even if you exclude energy production, US manufacturing output is crawling along.

Alongside slowing real output, inflation in prices of goods and services has disappeared in both the US and the Eurozone. Deflation is still close – another indicator of the long depression in the major economies.

But here is the real irony that should confound the Keynesians who reckon that the cause of the depression is the failure of governments raise spending to compensate for ‘weak demand’. Since 2008, the US economy has grown faster than the Eurozone. And yet in the US government spending has made a negative contribution to that growth while, despite all the talk of German-imposed austerity, government consumption has provided a net boost to real GDP in most European countries since the crisis broke. In other words, there has been more ‘austerity’ in the US than in Europe and yet the US economy has recovered better from the Great Recession!

The graph below shows that since 2008, the US economy has grown 10.8% but government spending (yellow bar) has shrunk, while the German economy has risen only 5.5% with government spending contributing over 2% pts of that. Even ‘austerity’ UK has seen more government spending in its recovery.

Nevertheless, the Keynesians continue to claim that this low growth world is due to the lack of fiscal and monetary injections into the economy andhas nothing to do with the underlying problems of the capitalist economy: low profitability, high debt and weak investment and poor productivity growth. Only this week, Martin Wolf told us, yet again, that weak growth in the Eurozone is due to the failure of Germans to spend or invest rather than save. Germany needs to absorb its ‘excess savings’ by spending to get Europe and the world going.

This is nonsense. As I explained in some detail in a previous post, there is not a global savings glut that needs to be absorbed. And German corporate savings as a share of GDP are not particularly high compared to other countries. The issue is low investment, yes. But why? Wolf seems to think it is due to ignorant, rigid attitudes in Germany and elsewhere. But the objective reason is low profitability from future investments and existing relatively high corporate debt. Another way of looking at this is to say that it is a ‘supply-side’ problem, not one of the lack of demand.

An argument in these terms has broken out between the Keynesians and the neo-classical wing of mainstream economics. A new paper by some top Keynesian economists, couched in extremely obtuse mathematical models, seeks to show that the current weak US economy is due to the inability of central banks to get interest rates low enough to stimulate investment. The US economy is ‘zero-bound’ and so we have ‘secular stagnation’. This is the Summers-Krugman explanation of this long depression.

In response, neoclassical economist John Cochrane has shown that these assumptions are just unrealistic. “I read this paper as a brilliant negative result. It shows just how extreme the implicit assumptions are behind the policy blather. It shows just how empty the idea is, that our policy-makers understand any of this stuff at a scientific, empirically-tested level, and should take strong actions to offset the supposed problems these buzzwords allude to”. Cochrane’s alternative view is simple, he says. Interest rates are low because inflation is near zero. Growth is low because productivity growth is low. Productivity growth is low because investment growth is low so the productive potential of the US economy has fallen back. This is much closer to the Robert J Gordon explanation of the depression.

The policy conclusion of the Keynesian position is to pump yet more money into the banks and the economy (helicopter money next) and for governments to launch spending programmes. The neoclassical supply-side policy position is to make companies more efficient by cutting wages and employment and reduce the ‘regulation’ of the capitalist companies to allow the ‘market’ to work; while cut government spending to reduce the level of debt.

Neither option has worked or will work.

Explaining the last ten years: Keynes or Marx – who is right?

May 2, 2016

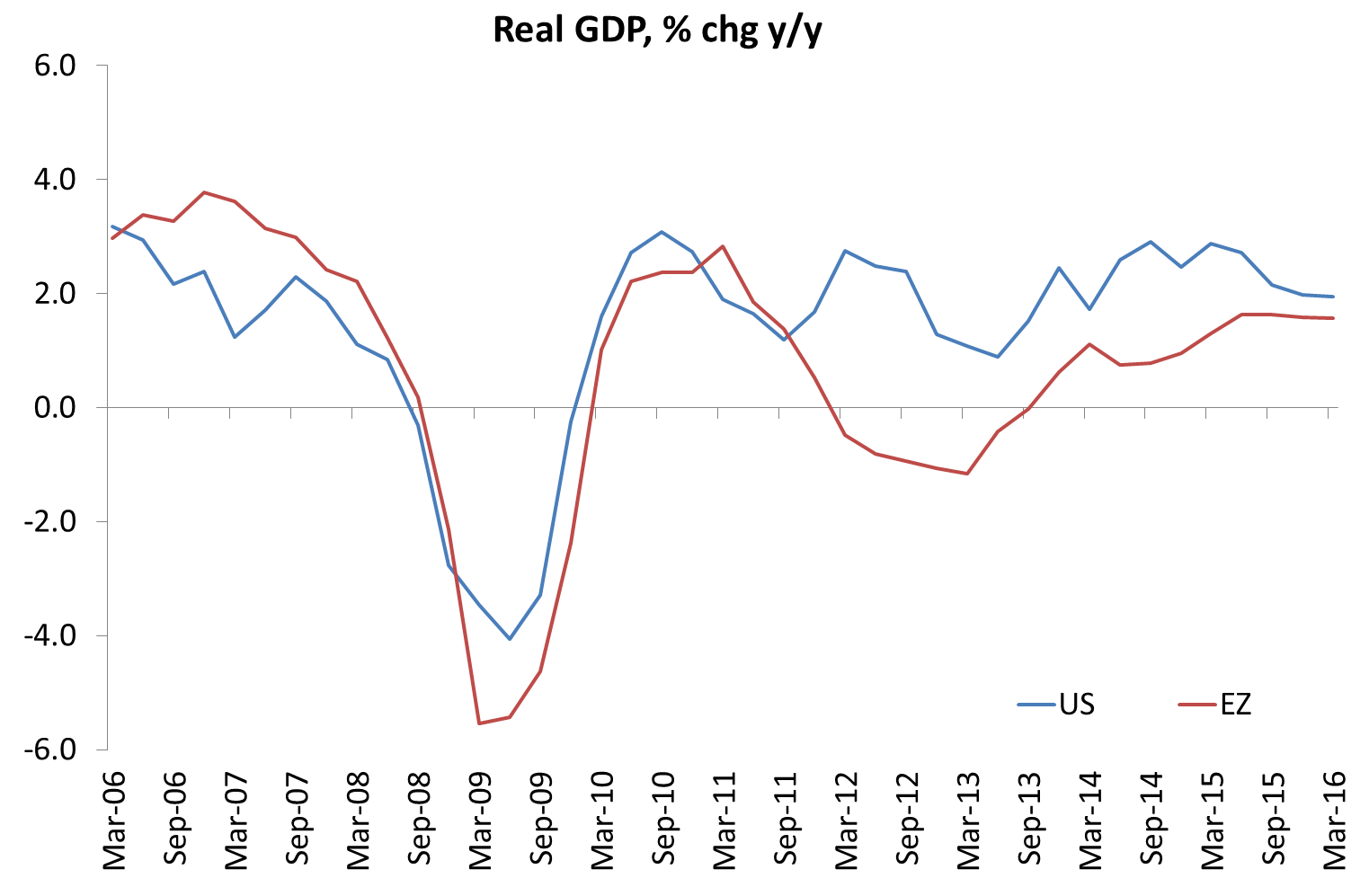

The latest economic data from the major capitalist economies do not make pretty reading. The global slowdown, as measured in real GDP growth, is worsening. The first reading for real GDP growth in the US, for the first quarter of 2016, delivered an annualised rise of just 0.5%, or 0.125% quarter over quarter. If we compare the size of the US economy after taking into account changes in prices (inflation), with the first quarter of 2015, then the American economy is larger by just 1.9%. That’s the slowest rate of expansion since early 2014. The US economy, the best of the major capitalist economies, is still just crawling along.

There was only one of the top seven capitalist economies (G7) apart from the US that was growing by more than 2% at the end of 2015. It was the UK. Now in the first quarter of 2016, the UK reported an expansion of just 0.4%, so that the British economy was larger by 2.1% compared to the first quarter of 2015. And most forecasters are expecting that growth rate to slip below 2% yoy in the current quarter we are now in (April to June).

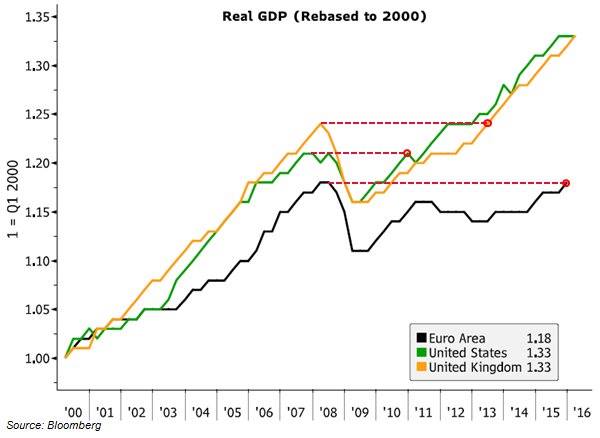

In the first quarter of 2016, the Eurozone group of economies grew faster than the US or the UK! The Euro area rose 0.55% compared to 0.4% in the UK and just 0.125% in the US. The EU region as a whole rose 0.5%. For the first time, Eurozone GDP in real terms has returned to its peak before the Great Recession – but three years after the UK and six years after the US! Compared to this time last year, Eurozone real GDP is up 1.53%. However, Eurozone growth has also slowed from 1.58% yoy in Q3 2015 to 1.55% in Q4 2015 and now 1.53%. It’s just that the US and the UK economies have slowed even more.

Now readers of my blog will know ad nauseam that this rate of growth in the major economies is an indication that the world economy remains in what I call a Long Depression (Jack Rasmus calls it an Epic Recession), where trend real growth is much lower than the long-term average and well below the rate of economic growth before the onset of the Great Recession in 2008-9. The latest quarterly figures for real GDP growth do no more than confirm that thesis.

Mainstream economics is reluctant to accept this view. Not only do the major official economic forecasters like the IMF, the OECD and EU Commission, after announcing yet another year of slow growth, keep forecasting a revival for the next year, but the consensus view is that the slowdown will end and growth will recover.

For example, Keynesian economist and former chief economist at Goldman Sachs,Gavyn Davies, now runs a forecasting agency, Fulcrum. Fulcrum and Davies told readers of the FT this week that, although real GDP figures are looking bad, GDP data look backwards, not forwards. And looking forward, things are getting better. Apparently, global activity is now only just below trend growth of 3.6% a year and the world economy has “again stepped back from the brink of outright recession”. So not to worry.

Moreover, there has been a move to dismiss the validity of the idea of GDP altogether as an indicator of prosperity or the health of the capitalist economy. The Economist magazine presented all the well-versed arguments for the weaknesses in the measurement of an economy using GDP: it does not measure the value of financial services properly, or the quality of new output and the gains of the new ‘disruptive technologies’ etc.

Many of these arguments may be right. But it is no accident that theEconomist wishes to dismiss the GDP measure only when it produces depressing results for capitalism. And GDP does provide a reasonable benchmark for ‘economic change’ over the long term, if not for ‘economic welfare’, i.e. the value and quality of living for the average person.

So if we work with the GDP data as we have it, we find confirmation of my view that we are in a Long Depression. The best measure of this, in my view, is real GDP (i.e. after inflation) per person. Real GDP per capita takes into account any expansion of population that would explain some growth in GDP just because of more people. This applies to countries like the UK where immigration from Europe has been considerable in the last ten years.

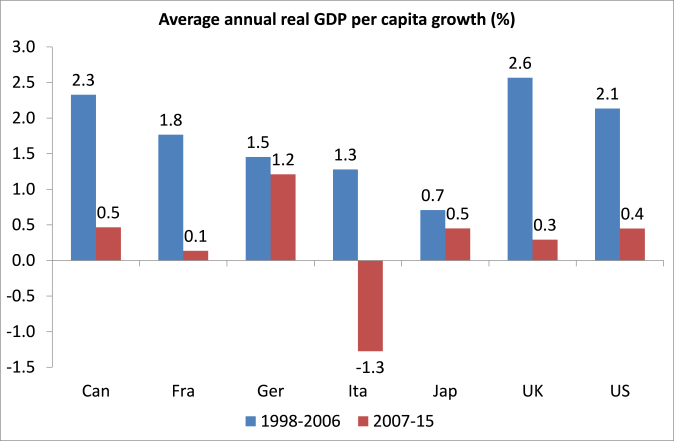

After a look at the data,I found that between 1998 and 2006, average annual growth in real GDP per person was much higher (1.5-2% a year) than between 2007 to now (under 0.5% a year) in all the major advanced capitalist economies. The change was particularly sharp in the US, the UK and the Eurozone, but less so in Japan (where the population has been falling). In Italy, real GDP per head has been negative since 2007 and France almost zero. So for nearly ten years, real GDP growth has been depressed way below previous averages.

In a recent post on his blogsite, British Keynesian economist, Simon Wren Lewis, now an adviser to the British opposition Labour Party, put up the question: how do we explain the last ten years of slow growth or depression?

According to Wren-Lewis, the cause of the depression is the after-effects of the Great Recession and the austerity policies of the governments subsequently. The Great Recession was caused by a ‘lack of demand’ I suppose, although Wren-Lewis is not clear on this. But no doubt he would agree with that other prominent Keynesian economist, Joseph Stiglitz, another ‘advisor’ to the British Labour party, who stated baldly at the time (2009) that “The lack of global aggregate demand is, in a sense, one of the fundamental problems underlying this crisis. Lack of aggregate demand was the problem with the Great Depression, just as lack of aggregate demand is the problem today.”

Now I have argued in this blog that to say the cause of the Great Recession was due to a lack of demand is bit like saying that that the cause of the streets being wet today is because it is raining today. That tells us nothing about why it is raining today and/or what causes rain to happen. Describing the Great Recession as a lack of demand is just that, a description, not an explanation.

But Wren-Lewis goes onto to consider why the Great Recession has morphed into a Long Depression. Apparently, it is partly because of the left-over effects of the Great Recession, but mostly because of ‘austerity’ measures by governments that has prolonged the recession instead of boosting government spending to get a recovery.

He admits that the last ten years have not turned out as the mainstream model might have expected, because this time, for some reason monetary policy has failed. “Here it is helpful to go through the textbook story of how a large negative demand shock should impact the global economy. Lower demand lowers output and employment. Workers cut wages, and firms follow with price cuts. The fall in inflation leads the central bank to cut real interest rates, which restores demand, employment and output to its pre-recession trend.”

But this time, interest rates have been taken to zero with little effect: the economies are zero-bound so more drastic action is needed. “We know why this time was different: monetary policy hit the zero lower bound (ZLB) and fiscal policy in 2010 went in the wrong direction.” This was a similar conclusion that Keynes himself reached when his easy monetary policy option also failed in the early 1930s.

Well, Marxist economics could have told the Keynesians that easy money would not do the trick. But it would also tell the likes of Wren-Lewis that‘reversing austerity’ will not either.

The implication of the Wren-Lewis position and that of all Keynesian explanations of the last ten years is that if governments had never adopted ‘neo-liberal’ policies of austerity, there would never be any recessions. But what if the cause of the Great Recession and the subsequent Long Depression is not the product of a ‘lack of demand’ as such or ‘pro-cyclical’ government spending policies (austerity) but is caused by a collapse of the capitalist sector, in particular, capitalist investment. And that investment collapsed because profitability in the capitalist sector fell, then the mass of profits fell, leading to investment, employment and incomes to fall, in that order. Then it’s the change in profits that leads to changes in investment and demand (consumption), not vice versa, as the Keynesians argue.

I have presented evidence for this cause of the cycle of boom and slump on this blog on many occasions. And to quote the latest empirical study by Jose Tapia Granados (a follow-up to this) “Data show that profits stop growing, stagnate, and then start falling a few quarters before the recession, when investment and wages start falling.” Tapia concludes that“The evidence is quite overwhelming that profits peak several quarters before the recession, while investment peaks almost immediately before the recession. Then profits recover before investment does, as illustrated by the investment trough that occurs around the end of the recession or the start of the expansion but following the profit trough for at least a few quarters”.

Currently, as I have shown, global corporate profits growth has dropped to near zero and in the US corporate profits are falling. If this is sustained, investment will contract and the major economies will drop into a new recession. Indeed, the most telling figure in the latest US GDP results was for business investment. In the first quarter of 2016, that fell 5.9% annualised, the biggest quarterly fall since the end of the Great Recession. For the first time, business investment was smaller than this time last year (by 0.4%). And even taking into account investment in housing and government, total investment fell. The fall in business investment has been mostly in energy and mining as oil prices collapsed – energy investment is down 75% since 2014!

Personal consumption growth ticked along at 2.7% yoy. Many mainstream economists argue that this is what matters in an economy because 70% of the economy is consumption. But in a capitalist economy, it is investment that decides, in particular business investment. If the negative trend in business investment continues, the US economy will not escape another recession.

The weird irony of the Keynesian/Wren-Lewis position is to argue that reducing profitability and profits (and thus raising wage share) should benefit the capitalist economy by raising consumption. Wren-Lewis notes the argument of fellow Keynesian Paul Krugman that high profit margins for US corporations might be a result of monopoly rents (control of the market) and if we get more ‘competition’, profit margins will fall to the benefit of all. I have dealt with the bogus mainstream argument in an article for the Jacobin online magazine.

As Wren-Lewis puts it, if profit margins fall back, that would be “an optimistic story, because an additional demand stimulus would increase wage but not price inflation, and we would see rapid growth in labour productivity as firms reversed their earlier labour for capital substitution.”

The Keynesian conclusion is that lower profits for capitalism will make capitalism work better because there will be more competition and less monopoly; and less profits means more wages and so more demand. The Marxist conclusion is the opposite: lower profitability and profits will lead to lower investment and productivity growth and a prolongation of the depression. Only a large destruction of capital values in a slump that restores profitability will create eventual recovery in a capitalist economy.

In effect, what the Keynesians want to see is an end to ‘neoliberal’ policies and their replacement by what used to be called ‘social democratic’ policies of government intervention to manage the capitalist economy and boost investment and demand. With this sort of help, capitalism can be restored to provide prosperity for the majority, as it was in the Golden Age of the 1960s when Keynesian policies ruled supreme.

This is the argument that Keynesian Brad Delong and his fellow author Stephen Cohen argue in their new book, Concrete Economics. It was also the argument presented by Brad Delong at this year’s conference of the American Economics Association (ASSA) when critiquing my own paper there on The Long Depression, the arguments of which he totally ignored.

It is a (Keynesian) myth that the brief Golden Age of fast growth, full employment and low inequality in the 1950s and 1960s was due to Keynesian economic policies. As I have shown on this blog and elsewhere, that brief period of capitalist success (confined to the advanced capitalist economies) was due to relatively high profitability of capital after the world war and the relative strengthening of the labour movement in conditions of relatively full employment that forced concessions from capital.

The subsequent neo-liberal period was not the result of right-wing governments ‘changing the rules of the game’, to use Joseph Stiglitz’s phrasing, but the crisis of falling profitability that necessitated new reactionary policies and governments to restore profits at the expense of labour. While profitability in the major economies remains near post-war lows, no amount of Keynesian monetary and fiscal policies will deliver a new ‘Golden Age’.

Brad Delong told us Marxist economists at ASSA that we are pessimists ‘waiting for Godot’, when capitalism can be made to work with the ‘concrete economics’ of Keynesian social democracy. Well, the last ten years cast doubt on that view and the next few years will see who is right.

There was only one of the top seven capitalist economies (G7) apart from the US that was growing by more than 2% at the end of 2015. It was the UK. Now in the first quarter of 2016, the UK reported an expansion of just 0.4%, so that the British economy was larger by 2.1% compared to the first quarter of 2015. And most forecasters are expecting that growth rate to slip below 2% yoy in the current quarter we are now in (April to June).

In the first quarter of 2016, the Eurozone group of economies grew faster than the US or the UK! The Euro area rose 0.55% compared to 0.4% in the UK and just 0.125% in the US. The EU region as a whole rose 0.5%. For the first time, Eurozone GDP in real terms has returned to its peak before the Great Recession – but three years after the UK and six years after the US! Compared to this time last year, Eurozone real GDP is up 1.53%. However, Eurozone growth has also slowed from 1.58% yoy in Q3 2015 to 1.55% in Q4 2015 and now 1.53%. It’s just that the US and the UK economies have slowed even more.

Now readers of my blog will know ad nauseam that this rate of growth in the major economies is an indication that the world economy remains in what I call a Long Depression (Jack Rasmus calls it an Epic Recession), where trend real growth is much lower than the long-term average and well below the rate of economic growth before the onset of the Great Recession in 2008-9. The latest quarterly figures for real GDP growth do no more than confirm that thesis.

Mainstream economics is reluctant to accept this view. Not only do the major official economic forecasters like the IMF, the OECD and EU Commission, after announcing yet another year of slow growth, keep forecasting a revival for the next year, but the consensus view is that the slowdown will end and growth will recover.

For example, Keynesian economist and former chief economist at Goldman Sachs,Gavyn Davies, now runs a forecasting agency, Fulcrum. Fulcrum and Davies told readers of the FT this week that, although real GDP figures are looking bad, GDP data look backwards, not forwards. And looking forward, things are getting better. Apparently, global activity is now only just below trend growth of 3.6% a year and the world economy has “again stepped back from the brink of outright recession”. So not to worry.

Moreover, there has been a move to dismiss the validity of the idea of GDP altogether as an indicator of prosperity or the health of the capitalist economy. The Economist magazine presented all the well-versed arguments for the weaknesses in the measurement of an economy using GDP: it does not measure the value of financial services properly, or the quality of new output and the gains of the new ‘disruptive technologies’ etc.

Many of these arguments may be right. But it is no accident that theEconomist wishes to dismiss the GDP measure only when it produces depressing results for capitalism. And GDP does provide a reasonable benchmark for ‘economic change’ over the long term, if not for ‘economic welfare’, i.e. the value and quality of living for the average person.

So if we work with the GDP data as we have it, we find confirmation of my view that we are in a Long Depression. The best measure of this, in my view, is real GDP (i.e. after inflation) per person. Real GDP per capita takes into account any expansion of population that would explain some growth in GDP just because of more people. This applies to countries like the UK where immigration from Europe has been considerable in the last ten years.

After a look at the data,I found that between 1998 and 2006, average annual growth in real GDP per person was much higher (1.5-2% a year) than between 2007 to now (under 0.5% a year) in all the major advanced capitalist economies. The change was particularly sharp in the US, the UK and the Eurozone, but less so in Japan (where the population has been falling). In Italy, real GDP per head has been negative since 2007 and France almost zero. So for nearly ten years, real GDP growth has been depressed way below previous averages.

In a recent post on his blogsite, British Keynesian economist, Simon Wren Lewis, now an adviser to the British opposition Labour Party, put up the question: how do we explain the last ten years of slow growth or depression?

According to Wren-Lewis, the cause of the depression is the after-effects of the Great Recession and the austerity policies of the governments subsequently. The Great Recession was caused by a ‘lack of demand’ I suppose, although Wren-Lewis is not clear on this. But no doubt he would agree with that other prominent Keynesian economist, Joseph Stiglitz, another ‘advisor’ to the British Labour party, who stated baldly at the time (2009) that “The lack of global aggregate demand is, in a sense, one of the fundamental problems underlying this crisis. Lack of aggregate demand was the problem with the Great Depression, just as lack of aggregate demand is the problem today.”

Now I have argued in this blog that to say the cause of the Great Recession was due to a lack of demand is bit like saying that that the cause of the streets being wet today is because it is raining today. That tells us nothing about why it is raining today and/or what causes rain to happen. Describing the Great Recession as a lack of demand is just that, a description, not an explanation.

But Wren-Lewis goes onto to consider why the Great Recession has morphed into a Long Depression. Apparently, it is partly because of the left-over effects of the Great Recession, but mostly because of ‘austerity’ measures by governments that has prolonged the recession instead of boosting government spending to get a recovery.

He admits that the last ten years have not turned out as the mainstream model might have expected, because this time, for some reason monetary policy has failed. “Here it is helpful to go through the textbook story of how a large negative demand shock should impact the global economy. Lower demand lowers output and employment. Workers cut wages, and firms follow with price cuts. The fall in inflation leads the central bank to cut real interest rates, which restores demand, employment and output to its pre-recession trend.”

But this time, interest rates have been taken to zero with little effect: the economies are zero-bound so more drastic action is needed. “We know why this time was different: monetary policy hit the zero lower bound (ZLB) and fiscal policy in 2010 went in the wrong direction.” This was a similar conclusion that Keynes himself reached when his easy monetary policy option also failed in the early 1930s.

Well, Marxist economics could have told the Keynesians that easy money would not do the trick. But it would also tell the likes of Wren-Lewis that‘reversing austerity’ will not either.

The implication of the Wren-Lewis position and that of all Keynesian explanations of the last ten years is that if governments had never adopted ‘neo-liberal’ policies of austerity, there would never be any recessions. But what if the cause of the Great Recession and the subsequent Long Depression is not the product of a ‘lack of demand’ as such or ‘pro-cyclical’ government spending policies (austerity) but is caused by a collapse of the capitalist sector, in particular, capitalist investment. And that investment collapsed because profitability in the capitalist sector fell, then the mass of profits fell, leading to investment, employment and incomes to fall, in that order. Then it’s the change in profits that leads to changes in investment and demand (consumption), not vice versa, as the Keynesians argue.

I have presented evidence for this cause of the cycle of boom and slump on this blog on many occasions. And to quote the latest empirical study by Jose Tapia Granados (a follow-up to this) “Data show that profits stop growing, stagnate, and then start falling a few quarters before the recession, when investment and wages start falling.” Tapia concludes that“The evidence is quite overwhelming that profits peak several quarters before the recession, while investment peaks almost immediately before the recession. Then profits recover before investment does, as illustrated by the investment trough that occurs around the end of the recession or the start of the expansion but following the profit trough for at least a few quarters”.

Currently, as I have shown, global corporate profits growth has dropped to near zero and in the US corporate profits are falling. If this is sustained, investment will contract and the major economies will drop into a new recession. Indeed, the most telling figure in the latest US GDP results was for business investment. In the first quarter of 2016, that fell 5.9% annualised, the biggest quarterly fall since the end of the Great Recession. For the first time, business investment was smaller than this time last year (by 0.4%). And even taking into account investment in housing and government, total investment fell. The fall in business investment has been mostly in energy and mining as oil prices collapsed – energy investment is down 75% since 2014!

Personal consumption growth ticked along at 2.7% yoy. Many mainstream economists argue that this is what matters in an economy because 70% of the economy is consumption. But in a capitalist economy, it is investment that decides, in particular business investment. If the negative trend in business investment continues, the US economy will not escape another recession.

The weird irony of the Keynesian/Wren-Lewis position is to argue that reducing profitability and profits (and thus raising wage share) should benefit the capitalist economy by raising consumption. Wren-Lewis notes the argument of fellow Keynesian Paul Krugman that high profit margins for US corporations might be a result of monopoly rents (control of the market) and if we get more ‘competition’, profit margins will fall to the benefit of all. I have dealt with the bogus mainstream argument in an article for the Jacobin online magazine.

As Wren-Lewis puts it, if profit margins fall back, that would be “an optimistic story, because an additional demand stimulus would increase wage but not price inflation, and we would see rapid growth in labour productivity as firms reversed their earlier labour for capital substitution.”

The Keynesian conclusion is that lower profits for capitalism will make capitalism work better because there will be more competition and less monopoly; and less profits means more wages and so more demand. The Marxist conclusion is the opposite: lower profitability and profits will lead to lower investment and productivity growth and a prolongation of the depression. Only a large destruction of capital values in a slump that restores profitability will create eventual recovery in a capitalist economy.

In effect, what the Keynesians want to see is an end to ‘neoliberal’ policies and their replacement by what used to be called ‘social democratic’ policies of government intervention to manage the capitalist economy and boost investment and demand. With this sort of help, capitalism can be restored to provide prosperity for the majority, as it was in the Golden Age of the 1960s when Keynesian policies ruled supreme.

This is the argument that Keynesian Brad Delong and his fellow author Stephen Cohen argue in their new book, Concrete Economics. It was also the argument presented by Brad Delong at this year’s conference of the American Economics Association (ASSA) when critiquing my own paper there on The Long Depression, the arguments of which he totally ignored.

It is a (Keynesian) myth that the brief Golden Age of fast growth, full employment and low inequality in the 1950s and 1960s was due to Keynesian economic policies. As I have shown on this blog and elsewhere, that brief period of capitalist success (confined to the advanced capitalist economies) was due to relatively high profitability of capital after the world war and the relative strengthening of the labour movement in conditions of relatively full employment that forced concessions from capital.

The subsequent neo-liberal period was not the result of right-wing governments ‘changing the rules of the game’, to use Joseph Stiglitz’s phrasing, but the crisis of falling profitability that necessitated new reactionary policies and governments to restore profits at the expense of labour. While profitability in the major economies remains near post-war lows, no amount of Keynesian monetary and fiscal policies will deliver a new ‘Golden Age’.

Brad Delong told us Marxist economists at ASSA that we are pessimists ‘waiting for Godot’, when capitalism can be made to work with the ‘concrete economics’ of Keynesian social democracy. Well, the last ten years cast doubt on that view and the next few years will see who is right.

No hay comentarios:

Publicar un comentario