Market turmoil

August 24, 2015

As I write on Monday 24 August, stock markets around the world are taking another plunge. Most markets have already fallen by 10% in the last month. Why is this happening?

The reasons are clear. The Chinese economy, now officially the largest in the world (at least as measured by the IMF’s rather weird purchasing power parity method), is slowing fast. Every bit of data coming out of China shows a worsening situation for manufacturing output, investment, exports and, above all, the purchase of raw materials from other countries. The drop in demand from China for basic commodities has caused a huge drop in commodity prices (the prices for oil, food, iron, coal, industrial metals etc). This drop in prices means less export sales for the likes of Brazil, Australia, Indonesia, Argentina etc. Also the Chinese are not buying so many BMWs, luxury handbags, machine tools, cars etc at home and abroad. That’s bad news for Europe and Japan, as well as the US.

The other cause is that, in addition to the global slowdown in so-called ‘emerging economies’, economic recovery in the ‘mature’ capitalist economies remains weak and in some cases looks to have run out of steam. The US economy has done the best since the end of the Great Recession in mid-2009. But it is still managing barely more than 2% real GDP growth a year and its manufacturing sector is dropping back.

The Eurozone economy is barely growing and that is only because Germany, the main economic powerhouse, has been able to recover somewhat. The rest of the Eurozone is stagnating and in some cases (Finland, Greece), it is still contracting.

Japan, supposedly set to boom under the policies of ‘Abenomics’, named after the Japanese prime minister Abe’s measures of cheap money from the central bank, government spending and neo-liberal reforms of labour rights, has failed to recover much at all. Strong and sustained economic growth in the major capitalist economies remains a mirage.

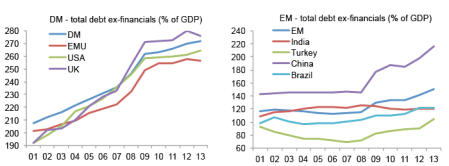

Another problem is the very strong dollar. Banks and financial institutions worried about economic growth elsewhere and looking for higher profits in a safe economy have flooded into buying dollar assets. And as the oil price falls (and it is priced in dollars), more capital has flowed into dollars to compensate. But this has led to a sharp fall in the value of other currencies. Many corporations around the world have borrowed in dollars and get revenues in their national currencies. So corporate debt bills in emerging economies are rising. Many corporations see less revenue growth ahead but bigger debts. So there is a serious prospect of a corporate debt crisis.

This exposes a big truth about the global ‘economic recovery’, such as it is, since 2009. It has been mainly based, not on investment in productive sectors to raise productivity and employment, but in fictitious capital,buying back shares, buying government and corporate bonds and property. Cheap and unending money from central banks in theirquantitative easing (QE) programmes has restored the banking system, but not the productive part of the capitalist economies.

Even central bankers are starting to doubt whether QE has done much good. Stephen Williamson,vice-president of the Federal Reserve Bank of St Louis, has just issued a study in which he concludes : “There is no work, to my knowledge, that establishes a link from QE to the ultimate goals of the Fed – inflation and real economic activity. Indeed casual evidence suggests that QE has been ineffective.”

Debt has not been reduced overall and but extended in the corporate sectors of the major economies. There is still a huge layer of fictitious capital, as Marx called it. It is this that is now collapsing. It appears that global investors are beginning to realise that the ‘recovery’ is fictitious and is only on yet another credit-fuelled mirage.

The supporters of the latest credit bubble, like Ben Bernanke, the former head of the US Federal Reserve, and Larry Summers, the ‘secular stagnation’ guru , are worried. In the FT today, Summers writes that “a reasonable assessment of current conditions suggest that raising rates in the near future would be a serious error”.

The Federal Reserve had been set to start to hike interest rates at the end of this year because the US economic recovery was now assured. I have stated in previous posts here the risk that this posed to the global economy if it was still in what I call a Long Depression (not the same as secular stagnation). Summers too is concerned. But what does he propose that the US policy makers do about it?

Summers simply calls for a continuation of the low interest rate policy that has so far signally failed to restore economic growth and instead has merely fueled a credit boom and rising inequality of income and wealth. “Satisfactory growth, if it can be achieved, requires very low interest rates that historically we have only seen during economic crises.” So it’s cheap money forever for Summers. Summers does say that there should be other measures: “such as steps to promote public and private investment”. But he provides no explanation of how investment is to raised by the capitalist sector in an environment where profitability is turning down globally despite the credit bubble. And where is the public investment?

The capitalist system needs to be cleansed of the fictitious capital built up under the policies of Bernanke and Summers and the central banks of the UK, Japan and now the ECB. It needs to deleverage not leverage more. The stock market is recognising that. Of course, ‘deleveraging’ would mean another major global slump to devalue capital and restore profitability in the productive sectors. That is the future that is getting closer.

The reasons are clear. The Chinese economy, now officially the largest in the world (at least as measured by the IMF’s rather weird purchasing power parity method), is slowing fast. Every bit of data coming out of China shows a worsening situation for manufacturing output, investment, exports and, above all, the purchase of raw materials from other countries. The drop in demand from China for basic commodities has caused a huge drop in commodity prices (the prices for oil, food, iron, coal, industrial metals etc). This drop in prices means less export sales for the likes of Brazil, Australia, Indonesia, Argentina etc. Also the Chinese are not buying so many BMWs, luxury handbags, machine tools, cars etc at home and abroad. That’s bad news for Europe and Japan, as well as the US.

The other cause is that, in addition to the global slowdown in so-called ‘emerging economies’, economic recovery in the ‘mature’ capitalist economies remains weak and in some cases looks to have run out of steam. The US economy has done the best since the end of the Great Recession in mid-2009. But it is still managing barely more than 2% real GDP growth a year and its manufacturing sector is dropping back.

The Eurozone economy is barely growing and that is only because Germany, the main economic powerhouse, has been able to recover somewhat. The rest of the Eurozone is stagnating and in some cases (Finland, Greece), it is still contracting.

Japan, supposedly set to boom under the policies of ‘Abenomics’, named after the Japanese prime minister Abe’s measures of cheap money from the central bank, government spending and neo-liberal reforms of labour rights, has failed to recover much at all. Strong and sustained economic growth in the major capitalist economies remains a mirage.

Another problem is the very strong dollar. Banks and financial institutions worried about economic growth elsewhere and looking for higher profits in a safe economy have flooded into buying dollar assets. And as the oil price falls (and it is priced in dollars), more capital has flowed into dollars to compensate. But this has led to a sharp fall in the value of other currencies. Many corporations around the world have borrowed in dollars and get revenues in their national currencies. So corporate debt bills in emerging economies are rising. Many corporations see less revenue growth ahead but bigger debts. So there is a serious prospect of a corporate debt crisis.

This exposes a big truth about the global ‘economic recovery’, such as it is, since 2009. It has been mainly based, not on investment in productive sectors to raise productivity and employment, but in fictitious capital,buying back shares, buying government and corporate bonds and property. Cheap and unending money from central banks in theirquantitative easing (QE) programmes has restored the banking system, but not the productive part of the capitalist economies.

Even central bankers are starting to doubt whether QE has done much good. Stephen Williamson,vice-president of the Federal Reserve Bank of St Louis, has just issued a study in which he concludes : “There is no work, to my knowledge, that establishes a link from QE to the ultimate goals of the Fed – inflation and real economic activity. Indeed casual evidence suggests that QE has been ineffective.”

Debt has not been reduced overall and but extended in the corporate sectors of the major economies. There is still a huge layer of fictitious capital, as Marx called it. It is this that is now collapsing. It appears that global investors are beginning to realise that the ‘recovery’ is fictitious and is only on yet another credit-fuelled mirage.

The supporters of the latest credit bubble, like Ben Bernanke, the former head of the US Federal Reserve, and Larry Summers, the ‘secular stagnation’ guru , are worried. In the FT today, Summers writes that “a reasonable assessment of current conditions suggest that raising rates in the near future would be a serious error”.

The Federal Reserve had been set to start to hike interest rates at the end of this year because the US economic recovery was now assured. I have stated in previous posts here the risk that this posed to the global economy if it was still in what I call a Long Depression (not the same as secular stagnation). Summers too is concerned. But what does he propose that the US policy makers do about it?

Summers simply calls for a continuation of the low interest rate policy that has so far signally failed to restore economic growth and instead has merely fueled a credit boom and rising inequality of income and wealth. “Satisfactory growth, if it can be achieved, requires very low interest rates that historically we have only seen during economic crises.” So it’s cheap money forever for Summers. Summers does say that there should be other measures: “such as steps to promote public and private investment”. But he provides no explanation of how investment is to raised by the capitalist sector in an environment where profitability is turning down globally despite the credit bubble. And where is the public investment?

The capitalist system needs to be cleansed of the fictitious capital built up under the policies of Bernanke and Summers and the central banks of the UK, Japan and now the ECB. It needs to deleverage not leverage more. The stock market is recognising that. Of course, ‘deleveraging’ would mean another major global slump to devalue capital and restore profitability in the productive sectors. That is the future that is getting closer.

No hay comentarios:

Publicar un comentario